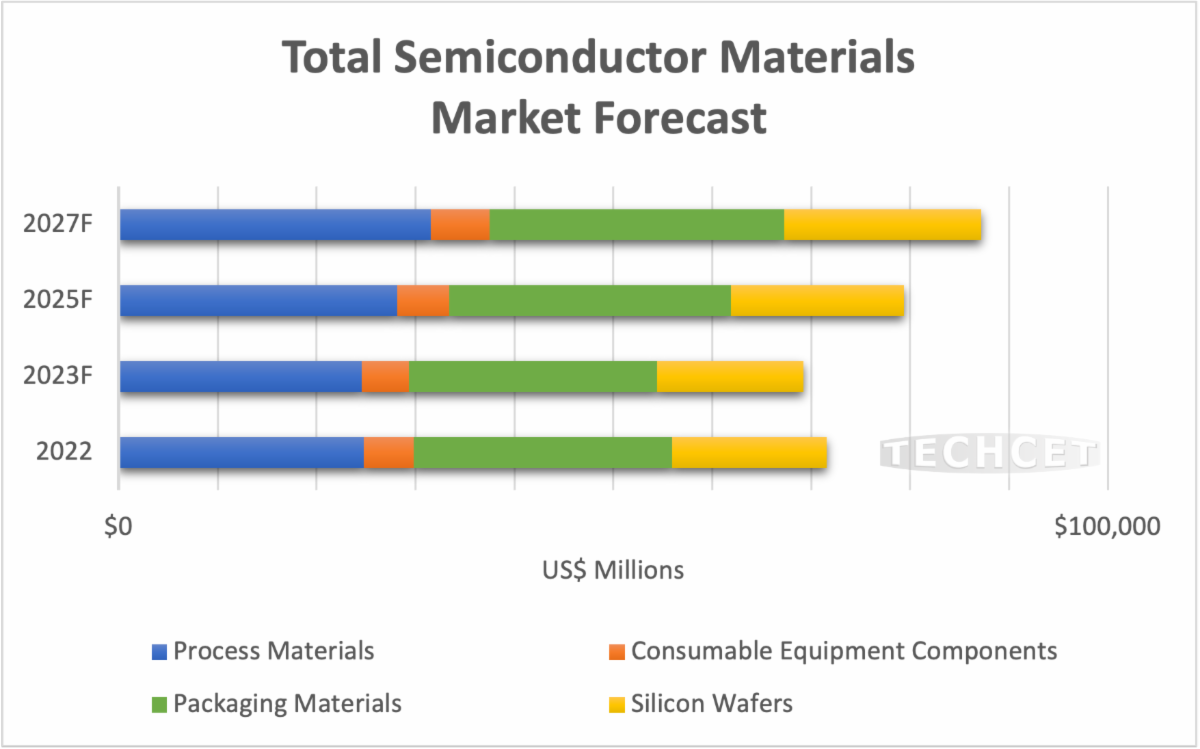

According to market and supply chain information, it is expected that the entire semiconductor materials market will rebound in 2024, growing by nearly 7% to reach $74 billion. Due to the overall slowdown in the semiconductor industry and a decrease in wafer production, there was a -3.3% contraction in 2023, followed by this upward shift. Looking ahead, the entire semiconductor material market is expected to grow at a compound annual growth rate of over 5% from 2023 to 2027. By 2027, it is expected that the market will reach $87 billion or more, and the expansion of new global wafer fabs will contribute to a potentially larger market size.

Although the economic slowdown in 2023 has eased supply constraints, the tight supply of 300mm wafers, epitaxial wafers, some specialty gases, and copper alloy targets is expected to recover in 2024 with the increase of new global wafer fabs. The degree of supply tightness will depend on the function of material supplier expansion delay.

If the material/chemical production capacity cannot keep up with the expansion of wafer factories, strong demand growth may put pressure on the supply chain. In addition to the expansion of global wafer fabs, new device technologies will also drive the growth of the materials market, as the number of layers increases, all gate field-effect transistors (GAA-FET), 3DDRAM, and 3DNAND require new materials and additional process steps. These materials include special gases for EPI silicon/silicon germanium, EUV photoresists and developers, CVD and ALD precursors, CMP consumables, and cleaning chemicals (including highly selective nitride etching).

The past five years have been a particularly turbulent period for the semiconductor industry. The increasingly tense trade war between the United States and China has led to technological restrictions and complete bans between the two countries. The sanctions imposed by the United States on Huawei in 2019 led to Huawei choosing to stockpile components to prevent disconnection from its major semiconductor suppliers.

The United States and its allies believe that China is importing advanced chip technology crucial for the development of artificial intelligence from the West, which can be used for various military purposes. Therefore, chip manufacturing has become the main focus of geopolitical tensions in 2023, when the United States and several other countries implement sanctions to curb the export of chip related technologies to China.

In response, China has restricted the export of gallium and germanium, which are crucial for semiconductor manufacturing

Although the chip war between the United States and China became a focal point last year, these tensions can be traced back to earlier times when the Covid-19 pandemic broke out. The closure of many factories worldwide, especially those with the majority of global supply coming from Asia, has brought additional pressure to the semiconductor industry.

Due to severe chip shortages, many companies have started stockpiling chips to increase inventory, while some Western participants have developed their own national strategies and laws (such as the EU Chip Act) to increase semiconductor production in this area. However, in the second half of 2023, demand for certain chip related products decreased, and many companies tightened their spending, resulting in oversupply in the global market.

The semiconductor industry will move towards a strong year of 2024

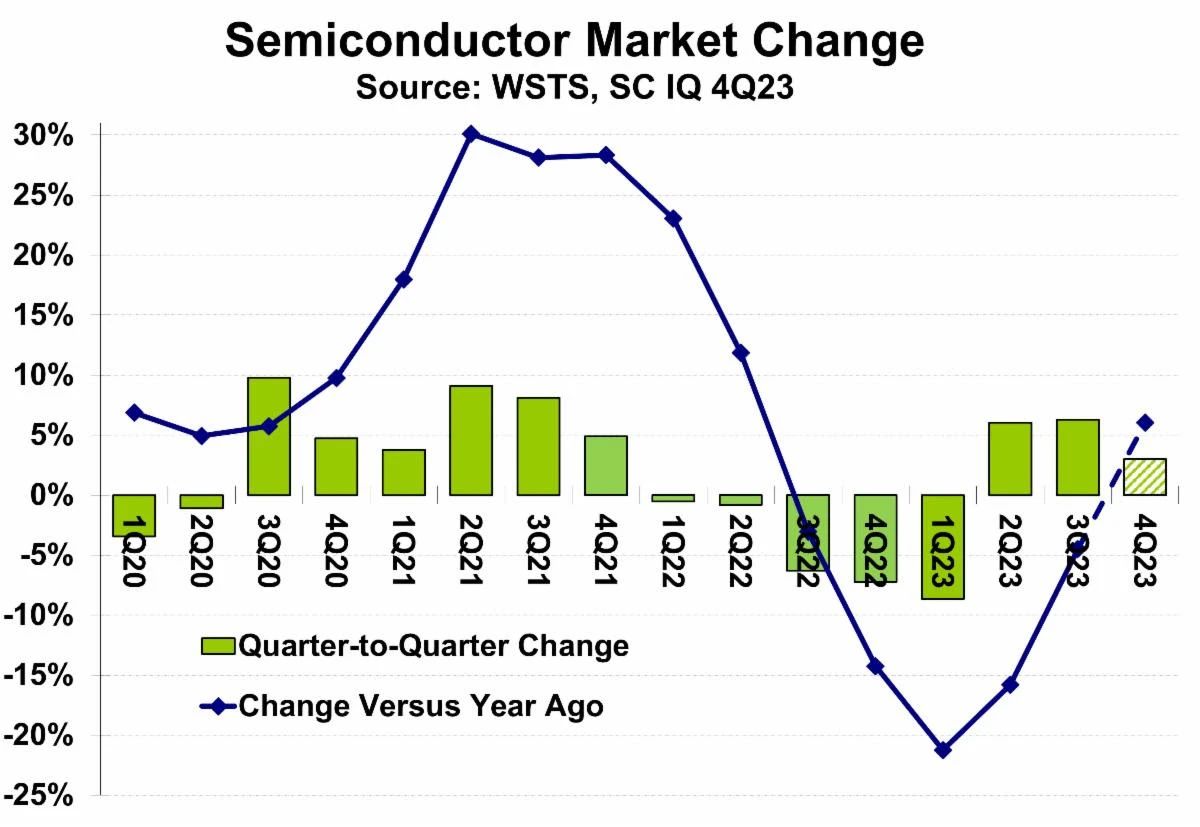

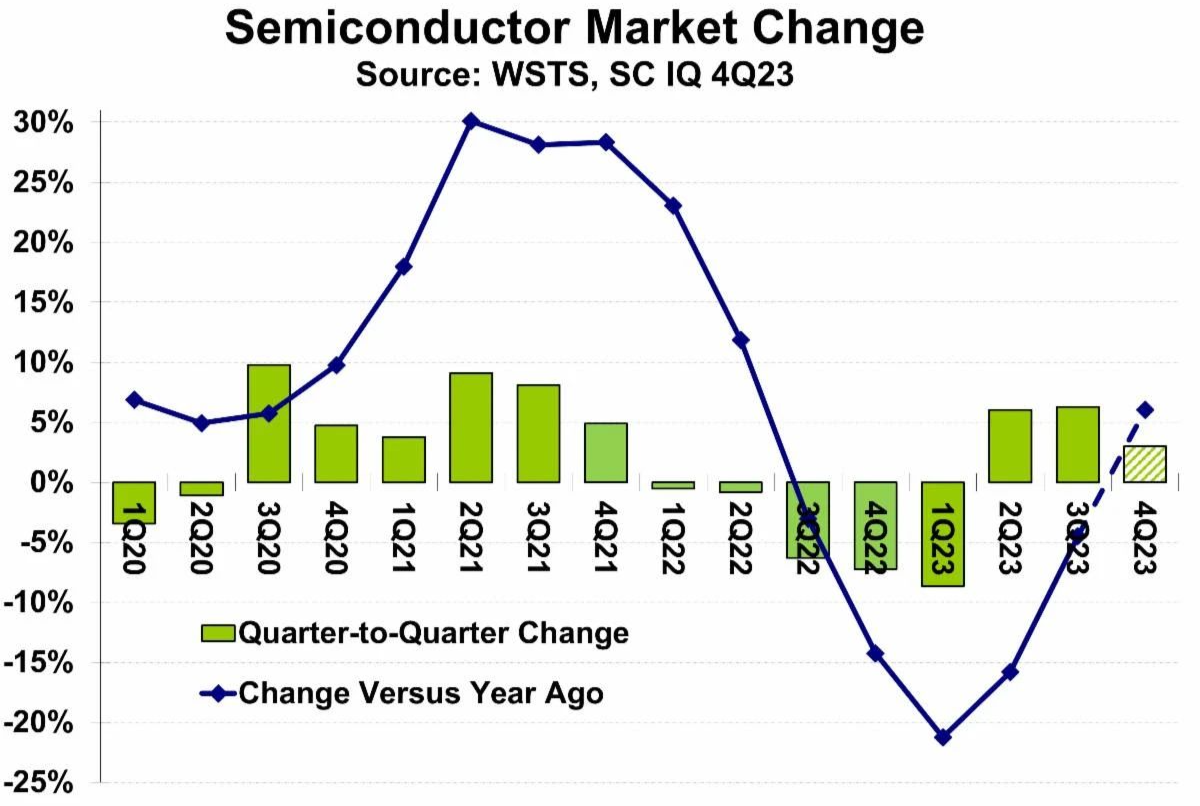

According to Pitchbook's data, venture capital in the semiconductor market has been on a downward trend, falling to a total of $10.3 billion in 2023, $12.8 billion in 2022, and $16.1 billion in 2021. Fortunately, although 2023 is a year for the industry to strive for a balance between famine and feasts, industry experts estimate that the semiconductor market will recover with a growth rate between 13% and 20%.

According to the latest research by IDC, with the explosive growth in global demand for artificial intelligence (AI) and high-performance computing (HPC), coupled with the stabilizing demand for flexible growth in the smartphone, personal computer, infrastructure, and automotive industries; The semiconductor industry is expected to usher in a new wave of growth. Semiconductor products cover logic integrated circuits (ICs), analog ICs, microprocessors and microcontroller ICs, as well as memory.

"The strict control of supply and production by memory manufacturers has led to price increases starting from early November, and the demand for artificial intelligence in all major applications will drive the overall semiconductor sales market to recover in 2024. Galen Zeng, Senior Research Manager for Semiconductor Research in the Semiconductor Supply Chain, including Design and IDC Asia Pacific, said, 'The manufacturing, packaging, and testing industries will bid farewell to the downturn in 2023.'

#1: The semiconductor sales market is expected to recover in 2024, with an annual growth rate of 20%

Due to weak market demand, the process of inventory consumption in the supply chain is still ongoing. Despite some sporadic short orders and rush orders in the second half of 2023, it is still difficult to reverse the annual decline of 20% in the first half of the year. Therefore, it is expected that the semiconductor sales market will continue to decline by 12% in 2023. The memory market will experience a recession of over 40% in 2023, and the production reduction effect in 2024 will drive up product prices. In addition, the increase in high priced HBM penetration rate is expected to become a driving force for market growth. With the gradual recovery of demand for smartphones and strong demand for AI chips, IDC predicts that the semiconductor market will resume its growth trend in 2024, with an annual growth rate of over 20%.

#2: ADAS (Advanced Driver Assistance Systems) and Information Entertainment Systems Drive the Development of the Automotive Semiconductor Market

Although the growth of the automotive market remains resilient, the clear trend of automotive intelligence and electrification is an important driving force for the future semiconductor market. ADAS holds the largest share of the automotive semiconductor market, with a compound annual growth rate (CAGR) of 19.8% by 2027, accounting for 30% of the automotive semiconductor market that year. Information entertainment occupies the second largest share of the automotive semiconductor market, with a compound annual growth rate of 14.6% by 2027, accounting for 20% of the market that year, driven by automotive intelligence and connectivity. Overall, more and more automotive electronics will rely on chips, which means that the demand for semiconductors will be long-term and stable.

#3: Expanding Semiconductor Artificial Intelligence Applications from Data Centers to Personal Devices

The reason why artificial intelligence has caused a sensation is that data centers require higher computing power, data processing, complex big language models, and big data analysis. With the advancement of semiconductor technology, it is expected that starting from 2024, more AI functions will be integrated into personal devices, and AI smartphones, AIPCs, and AI wearable devices will gradually be pushed to the market. It is expected that with the introduction of artificial intelligence, more innovative applications will emerge in personal devices, which will actively stimulate the demand for semiconductors and advanced packaging.

#4: IC design inventory consumption is gradually ending, and the Asia Pacific market is expected to grow by 14% by 2024

Despite the relatively sluggish performance of IC designers in the Asia Pacific region in 2023 due to long-term inventory rationalization, most suppliers still maintain resilience under market pressure. Every supplier actively invests and innovates to maintain their position in the supply chain. In addition, IC design companies continue to cultivate technology through the adoption of client devices and artificial intelligence in automobiles. With the gradual recovery of the global personal device market, new growth opportunities will emerge, and it is expected that the overall market will grow by 14% annually in 2024.

#5: The demand for advanced processes in the casting industry has surged

The wafer foundry industry has been affected by inventory adjustments and weak demand, resulting in a significant decrease in capacity utilization in 2023, especially in mature process technologies above 28 nanometers. However, due to the rebound in demand for some consumer electronics and AI, the recovery of 12 inch wafer fabs was slow in the second half of 2023, with the recovery of advanced processes being the most significant. Looking ahead to 2024, with the efforts of TSMC, Samsung, and Intel, as well as the gradual stabilization of end-user demand, the market will continue to rise. It is expected that the global semiconductor foundry industry will achieve double-digit growth next year.

#6: The growth of China's production capacity and intensified price competition for mature processes

Under the influence of the US ban, China has been actively expanding production capacity. In order to maintain capacity utilization, the Chinese industry continues to provide preferential pricing, which is expected to bring pressure to "non Chinese" contract factories. In addition, industrial control and automotive ICs must be destocked in the short term from the second half of 2023 to the first half of 2024, as wafer production is mainly focused on mature processes, which will continue to put pressure on suppliers and their ability to regain bargaining power.

#7: The compound annual growth rate of the 2.5/3D packaging market is expected to be 22% from 2023 to 2028

With the increasing requirements for the functionality and performance of semiconductor chips, advanced packaging technology has become increasingly important. The 2.5/3D packaging market is expected to grow at a compound annual growth rate of 22% from 2023 to 2028, making it a highly focused area in the semiconductor packaging testing market.

#8: CoWoS supply chain capacity has doubled, increasing AI chip supply

The AI wave has driven a surge in server demand, which relies on TSMC's advanced packaging technology CoWoS. At present, there is still a 20% gap in the supply and demand of CoWoS. In addition to NVIDIA, orders from international IC design companies are also increasing. It is expected that CoWoS production capacity will increase by 130% by the second half of 2024, and more manufacturers will actively enter the CoWoS supply chain, which is expected to make AI chip supply stronger in 2024 and an important growth booster for the development of artificial intelligence applications.

Air Separation Plant/Nitrous oxide plant/CO2 recovery plant/Acetylene Plant/Mobile Tank/ISO Tank Container/Cryogenic Storage Tank/LPG Storage Tank/Cryogenic Pump/Micro Bulk Tank Solutions/Cryogenic Semi Trailer Transport Tanker/LPG Semi Trailer Tanker/Dewar Flask/Vaporizer/Cylinders/Dry ice making machine/Calcium Carbide

Product series : Air Separation Plant | Cryogenic Storage Tanks | ISO tanks | Semi Trailer | Vaporizers | Pumps | Dewar Flasks| Dry Ice Machines | Cylinders